Financial sponsors were also active in the hospice industry either through new investments or current

hospice platforms. The Vistria Group sold its position in Agape Hospice to Ridgemont Equity Partners

shortly after Agape acquired Serenity Hospice. Coltala Holdings and Trive Capital invested in Choice

Health at Home, which then acquired Alpha Home Health and Hospice shortly after. Below, Westcove aggregated select hospice transactions completed in 2021 and YTD 2022:

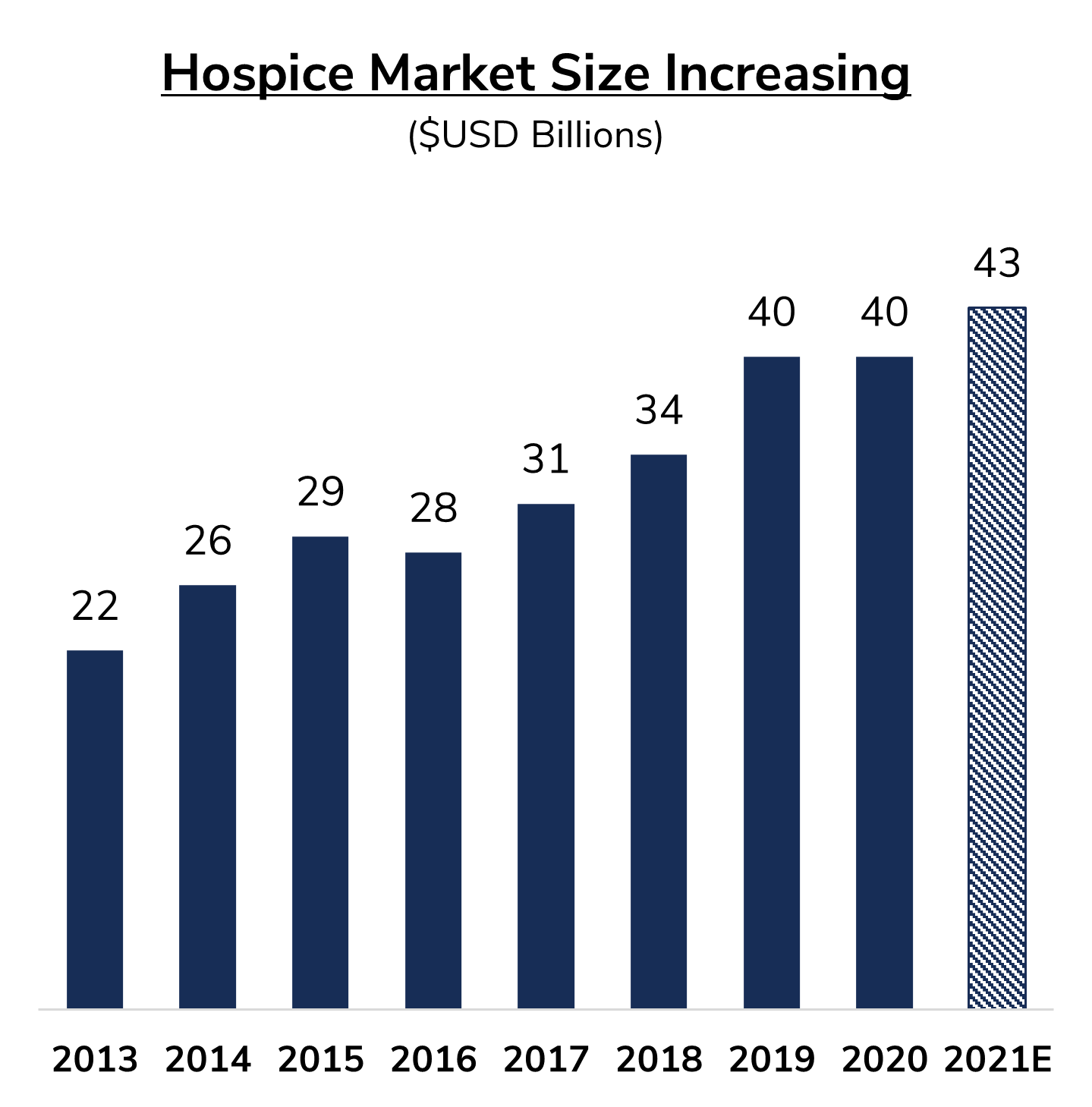

In addition to the longstanding drivers for consolidation, there were several regulatory developments that

came into effect in 2021 spurring additional growth and interest for hospice providers. The Medicare

Advantage “Carve-in” and increasing reimbursement rates drove higher valuations for hospice companies

relative to historical prices and other healthcare subindustries, such as home health care. The flurry of

activity shown on the previous page can in part be attributed to these regulatory dynamics.

Westcove continues to believe primary care and hospital referrals will continue to significantly increase

hospice utilization due to the “carve-in” supporting even greater industry growth in 2022 and beyond.

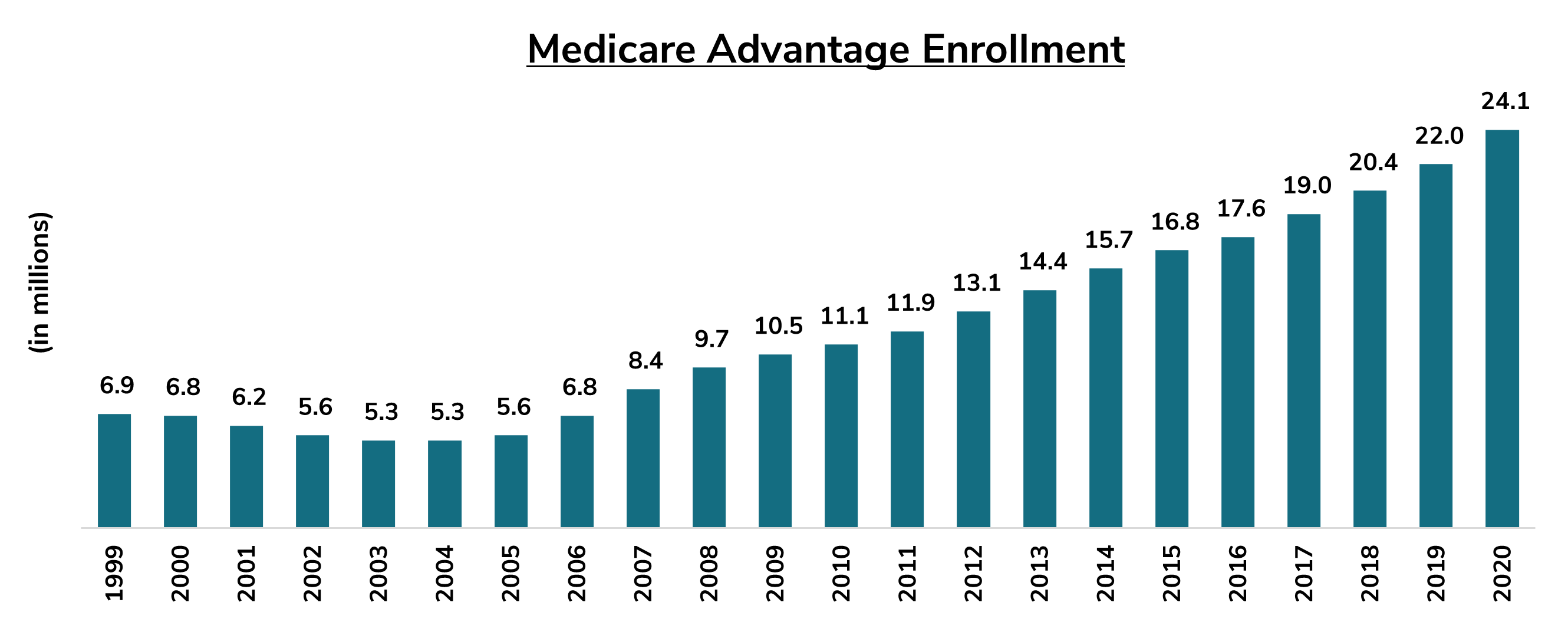

Medicare Advantage enrollment has grown rapidly over the last two decades, both in overall volume and

as a percentage of total Medicare Enrollment, as demonstrated in the chart above. Catering to this largely

untapped population will provide substantial tailwinds for hospice providers. This in turn will create more

demand and interest in hospice providers, further increasing lofty valuations.

The longstanding drivers of market fragmentation and increasing hospice utilization, coupled with

successful implementations of regulatory developments will continue to push an already active mergers

and acquisitions market for hospice providers to further all-time highs. COVID-19 has done little to cool

down the market, even with recent spikes due to the Omicron and Delta variants, significant hospice deals

have continued to successfully close such as the January 2022 Addus acquisition of JourneyCare. The

current market environment remains an ideal time for hospice providers to consider a transaction or

recapitalization. A transaction or recapitalization would allow hospice providers to maximize their equity

value at a time when the market is attractive for investors and strategic acquirers, leading to premium

valuations during competitive transaction processes.