Justin Hand

Managing Director

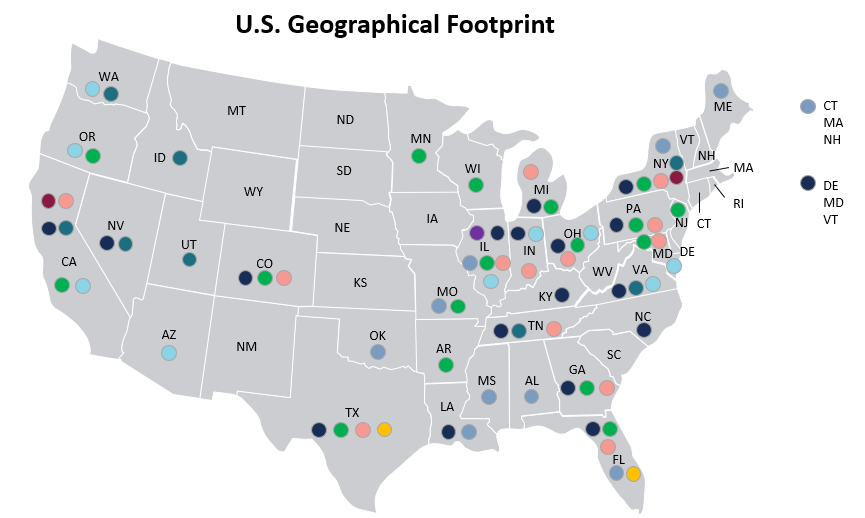

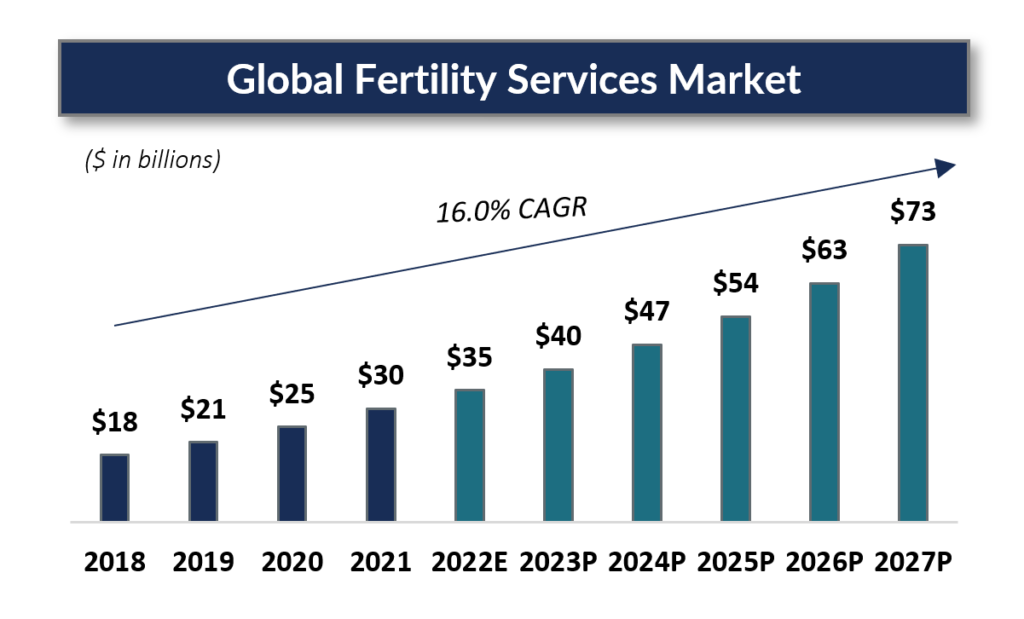

In recent years, the fertility services market has experienced a notable trend towards consolidation led by private equity’s first partnership in 2015, with TA Associates’ recapitalization of CCRM, which is now an affiliate of Unified Women’s Healthcare. The fertility services market in the United States alone has experienced an average annual growth rate of 3.8% from 2016 to 2021. Since then, there has been a steady increase in transactions with a total of nine private equity-backed platforms within the space. The continued consolidation is due to add-on acquisitions from independent fertility services practices that want to partner and join these larger, well-established networks. Recently, further consolidation has been driven by these larger, well-established networks that are seeking ancillary service lines, such as advanced genetics testing clinics, egg donation banks, and surrogacy agencies, to help bolster their ancillary service lines.  The addition of these ancillary service groups is attractive to these independent fertility practices because it allows these practices to provide highly personalized and holistic care while meeting the needs of the patients. As demand for fertility services increases across the country, the global fertility services market is projected to grow from $30 billion in 2021 to $73 billion in 2027, a CAGR of 16.0%. To meet and address this growth, these fertility services practices must consider a partnership that will provide them with the scale, resources, expanded service lines, and geographic reach to keep their competitive advantage in today’s changing market.

The addition of these ancillary service groups is attractive to these independent fertility practices because it allows these practices to provide highly personalized and holistic care while meeting the needs of the patients. As demand for fertility services increases across the country, the global fertility services market is projected to grow from $30 billion in 2021 to $73 billion in 2027, a CAGR of 16.0%. To meet and address this growth, these fertility services practices must consider a partnership that will provide them with the scale, resources, expanded service lines, and geographic reach to keep their competitive advantage in today’s changing market.